By: Nora Maene, Digital Media Solutions Marketing Director, Alcatel-Lucent

Global mobile traffic has increased with a factor of 30 in 5 years time; 6 billion mobile apps have been downloaded in 2010. Besides being a challenge, this explosive growth also presents an opportunity for communication service providers (CSPs) to engage in new ecosystems and business models – embracing cloud services and working with over-the-top players to transform application and content value chains.

Today, a large portion of the return for mobile applications comes from the mobile data revenues that they drive (growing from $260 billion in 2010 to $500 billion in 2015). Given that mobile data revenue is more than a 100-fold the revenues from mobile apps purchases, it is clear that stimulating mobile data consumption is the primary monetization vehicle for service providers.

With a need to increase mobile data usage - and changing market dynamics – it is clear that CSPs have to launch new application services in their markets as soon as possible to monetize the mobile application opportunity.

In order to shorten time-to-market, however, they need to do things differently - opening up their network assets for internal and third-party app developers so that the innovation demanded by the market can occur in a very flexible way.

In order to scale, CSPs also need to build a new ecosystem for apps, whether it is for their internal developers, their strategic partners or the large crowd of external app developers.

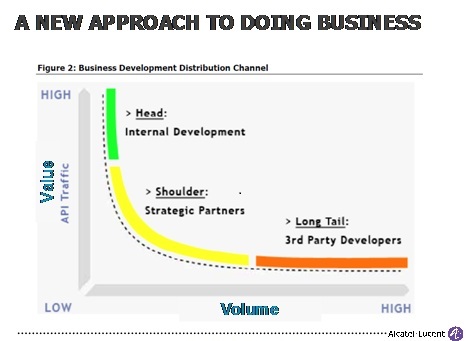

As a matter of fact, each of these three groups can be linked to a different zone in the hyperbolic “Value – Volume” graph of long tail apps and content services, in which we distinguish between three apps types: “head”, “shoulder” and “tail”. Each of these three types of apps demands a different go-to-market strategy by the CSP.

- The head of the curve - with a small number of high value apps – represents internally-developed apps and services that either address mass or niche markets. Examples include innovative communications services, mobile commerce services, or multiscreen video solutions that bring TV and video-on-demand to tablets and smartphones. Besides building brand equity, these apps typically help to increase customer loyalty and retention. Monetization of the “head” can happen in three ways: through the classic bundle of value added services with data access, through subscription services offered on top of the data plan for niche services, or through a co-branded offer (with a partner) for a short term highly targeted promotion.

- The shoulder of the Value-Volume apps curve is the middle zone - where both existing and new partners can help to address new vertical industry opportunities, such as healthcare, travel, finance, etc. For these apps, platform exposure and a high-touch collaboration is needed between the strategic partners and the CSP. A SaaS (software-as-a-service) model works well here, with a focus on simplified integration, easier on-boarding of external partners and reduced development time and cost. CSPs need to create an ecosystem where value is created for these partners as well, e.g. through co-branding. Monetization results from offering these more differentiated and personalized services, and through the use of multiple, flexible business models: from a simple pay-per-use model, a tiered user volume, or flat monthly fees.

- The long tail of apps only requires a low-touch strategy: the CSP “just” makes his network easily accessible for independent web, mobile and widget developers. This is more of a self-service model where simplicity is the key word, where the CSP offers capabilities in a wholesale model, and where new distribution channels can be created. Making it simple for developers to start using the network APIs is key to achieve mass adoption (by well documenting them, for instance). Usage-based pricing models work best here.

Although engaging long tail developers can enable innovation at the speed of ideas, this type of apps is also the most difficult one to get a grip on and should not be the main priority for the CSP when kicking off their apps strategy. The community of long tail app developers is very fragmented and scattered all over the world. Moreover, CSPs usually need to build the skills for exposing and documenting APIs in a simple way. As long tail apps are not generating large revenues in the short term, they should be part of a longer-term strategy – with the support from top management.

Alcatel-Lucent helps CSPs understand the challenges and opportunities associated with the rapid transformation of application and content value chains. It has a content-rich resource library where you can learn more about capitalizing on evolving ecosystems.