By: Josee Loudiadis, Director of Network Intelligence, Alcatel-Lucent

Voice over LTE (VoLTE) and rich communications services can help mobile service providers reclaim market share being lost to over-the-top (OTT) applications.

Voice and text revenues are declining as mobile service providers (MSPs) face an unprecedented challenge from OTT communication apps such as Facebook, Instagram, and lesser known entrants, including WhatsApp and LINE. At first, MSPs enjoyed net gains because the use of these apps had generated significant data revenue. But times have changed. While still a source of revenue, these apps have begun to erode MSP’s native voice and messaging revenue.

To illustrate, let’s look at WhatsApp, who recently debuted its business model for mobile virtual network operators. In this model, WhatsApp (now owned by Facebook) provides voice and messaging services while leasing wireless services from a mobile operator. This means that MSPs are left with price per bit as their sole differentiator.

What’s more, the massively popular OTT apps are generating ad revenue, giving them yet another advantage in their competition with MSPs who haven’t yet effectively exploited this revenue source. Fortunately, the tide is turning in favor of MSPs with the introduction VoLTE and rich communications services.

To help you prepare for a VoLTE launch, this blog series provides tips and insights on your go-to-market questions. You’ll also see how our Wireless Network Guardian’s network analytics capabilities can assist you with your launch strategy.

OTT voice-enabled apps: popularity assessment

There are several key apps in this sector whose popularity we’ve examined:

- LINE

- Viber

- Tango

- Skype

- Nimbuzz

- FaceTime

Each offers at least one voice feature, such as video calling, voice calling, or voice messaging. Much like VoLTE, these apps often combine voice features with texting or content sharing. This study situates their voice services within the overall voice-enabled communication package delivered by these apps.

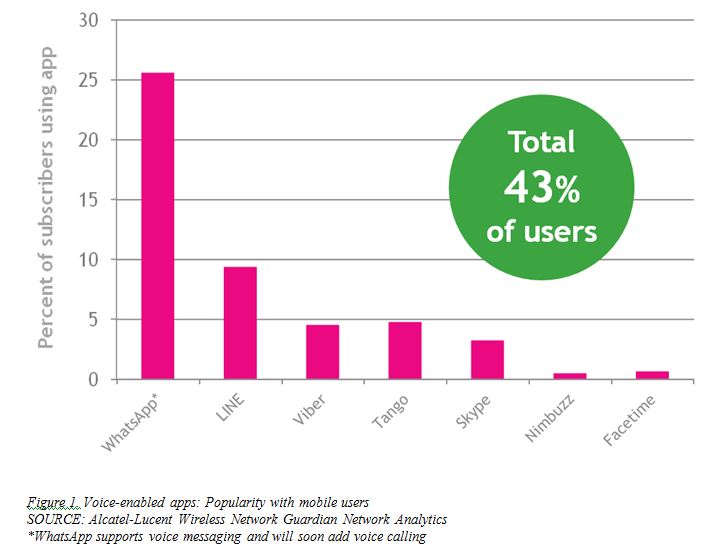

On average, 43% of subscribers worldwide make use of these OTT apps on mobile networks on a given month. But breaking it down by app is more revealing: their popularity ranges from less than 1% for Facetime and Nimbuzz to 26% for WhatsApp. Even more interesting is the fact that some subscribers use more than one OTT voice-enabled app. When adding the popularity of the individual apps, the sum is 68% – far exceeding the 43% reported above which represent the number of unique subscribers operating those apps.

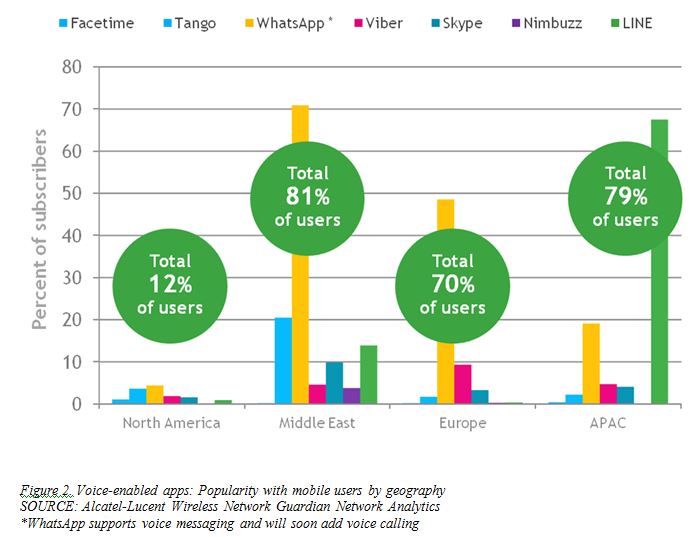

But this competitive landscape varies widely across geography, and indeed, even across different networks within the same country. Service providers in North America have little competition from OTT voice-enabled apps, since only 12% of subscribers, on average, make use of them. The most popular of these apps in North America is WhatsApp, reaching just over 4% of users. By comparison, Middle Eastern subscribers are especially active with OTT voice-enabled apps where 81% of subscribers make use of them. In fact, the cumulative sum of subscribers across those apps reaches 123% which means some subscribers use more than one of these apps! In that market, WhatsApp leads the pack by a wide margin with 71% of users hopping on it monthly.

By comparison, Middle Eastern subscribers are especially active with OTT voice-enabled apps where 81% of subscribers make use of them. In fact, the cumulative sum of subscribers across those apps reaches 123% which means some subscribers use more than one of these apps! In that market, WhatsApp leads the pack by a wide margin with 71% of users hopping on it monthly.

Europe and APAC have 70% and 79% of their users launching voice-enabled apps; but WhatsApp dominates in Europe whereas LINE dominates APAC. APAC is also home to the network with the most users for a given OTT voice-enabled app in this study: a record setting 85% made use of LINE.

OTT voice-enabled app usage

OTT apps are largely perceived as being “free”. Few users think about the data usage incurred by these apps since their bill only reports the total monthly data volume spent. How much is spent for each app is a total mystery for consumers and often for service providers too! But it is imperative to know how much data users spending on OTT voice-enabled apps to select the appropriate tariff strategy for VoLTE.

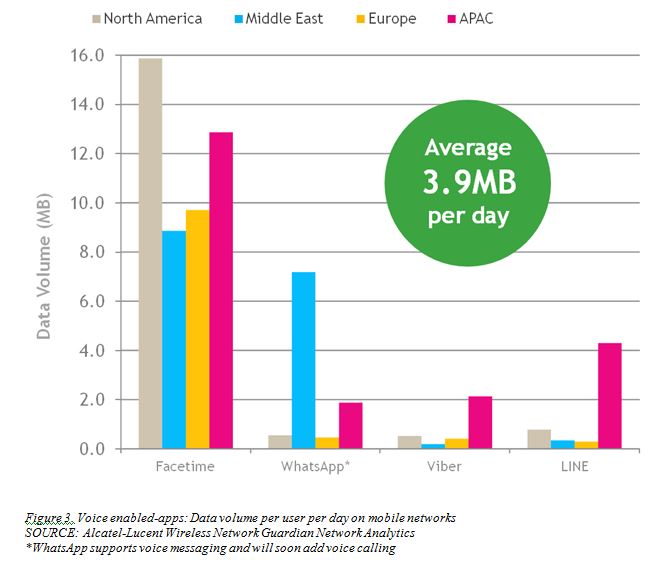

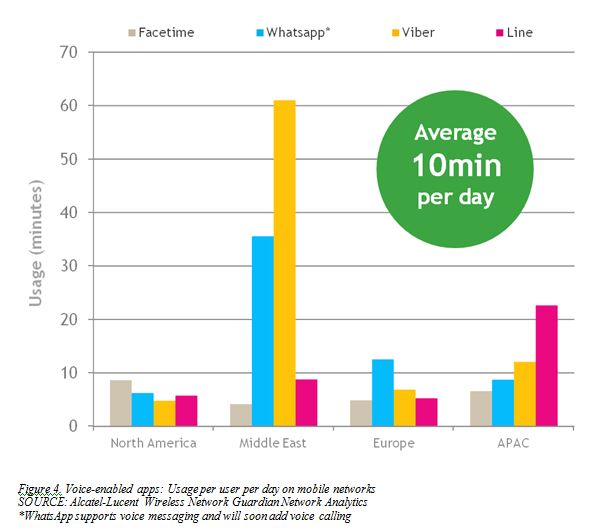

The average subscriber consumes 3.9 MB per day on these apps. That number includes all manners of communication offered by the app: voice messaging, video calling and texting. But that number differs greatly across apps and by geography. Facetime is by far the most data intensive with data volume of 12 MB per user per day on average. Its video call format drives data consumption much above other OTT voice-enabled apps who offer a range of less data intensive communication methods such as texting or audio phone calls. Another interesting observation: WhatsApp users in the Middle East and LINE in APAC consumed significantly more data than other app and geography combinations. This effect could be due to subscribers using the app often through the day, or to using data-heavy features. This distinction should be further investigated in a given mobile network before a VoLTE launch. The average by geography is also telling: APAC spends the most data with 5.3 MB per user per day on average. Some regions of APAC offer mostly unlimited data which may explain the difference. And while fewer subscribers in North America used OTT voice-enabled apps, the average consumption is close to the highest with 4.4 MB per user per day on average. This average is driven mainly by Facetime which tells us of North America’s propensity for video calls. The number of minutes of usage is another key piece of information for marketing strategy.

The average by geography is also telling: APAC spends the most data with 5.3 MB per user per day on average. Some regions of APAC offer mostly unlimited data which may explain the difference. And while fewer subscribers in North America used OTT voice-enabled apps, the average consumption is close to the highest with 4.4 MB per user per day on average. This average is driven mainly by Facetime which tells us of North America’s propensity for video calls. The number of minutes of usage is another key piece of information for marketing strategy.

On average, these OTT apps will see 10 minutes of usage per day. Those minutes represent the overall amount of time spent using the app, whether sending voice messages, video calling or texting. But users could be spending anywhere from 2-61 minutes depending on geography and specific networks.

Tariff strategies

And therein lies the fork in the road: should voice features be charged per minute as usual or is it time to ban minutes altogether in favor of data usage fees? Depending where one lives in the world, a VoLTE strategy will have different goals. In North America, it is about keeping subscribers from transitioning to OTT voice-enabled apps. In the Middle East and some locations in APAC, it is about enticing them back to the service provider’s app.

In North America, the trend has been to keep VoLTE rates identical to 3G: unlimited domestic minutes are included in the monthly plan. Given the limited competition from OTT voice-enabled apps in North America, the status quo for VoLTE voice calls makes sense. And video calling will be charged against the data plan – an excellent harbinger of healthy revenues to come given North America’s pre-disposition to video calling and the sharp data demand associated with that service.

In Europe and the Middle East, a different strategy might be required. To compete against WhatsApp and Viber, it might be necessary to meet them on their own turf and charge for data. VoLTE has been shown to require 10 times less bandwidth[1] – a marketing campaign touting that attribute in conjunction with the deployment of systems capable of reporting per app data consumption should lead users to make more educated choice towards the least expensive VoLTE option for voice calling.

While this blog focused on users’ affinity for alternate OTT voice-enabled apps, another attribute is key to a successful VoLTE launch: service quality. Mobile operators are in a position to deliver higher quality voice calls than their OTT competitors. Guaranteed quality could be an attractive proposition for enterprise users, especially while they try to access conference bridges or attend important calls while on the go.

Our Analytics Beat studies examine a representative cross-section of mobile data customers using the Alcatel-Lucent Wireless Network Guardian and are made possible by the voluntary participation of our customers. Collectively, these customers provide mobile service to millions of subscribers worldwide.

Footnote

[1] Signals Ahead Research “Behind the VoLTE curtain, part 1” reports 6 times fewer PDCCH (Physical Downlink Control Channel) grants, 4 times fewer transmissions, and 89% less signaling overhead.