Our sector of the marketplace - telecommunications - is about to undergo a change. Yeah, we have been in a shift for a good while, but more is coming.

We went from TDM to VoIP to Hosted PBX to UCaaS to UC&C.

We went from T1 to cable broadband to Gigabit.

The consolidation of cable will tighten the market in 15 to 18 months. (It takes that long for integrations to take hold.) Now if the integrations are not a big fail, then cable - New Charter/Spectrum, Comcast, Altice - will ratchet up the competition in the small business market for triple play.

"Cable/MSOs are the fastest growing providers in the business services market, with much of their recent success in the mid-size business space," reported MarketResearch. Think about that: the mid-sized space - not just the small business segment of the market.

Of the $104 Billion total businesses spent on telecom services in the US in 2014, AT&T had the largest share (33%), followed by Verizon (22%) and the rest of the LEC band of brothers (Level3, CenturyLink, Sprint, Windstream). MSOs have more than $12 Billion of that pie, with the lion share - $5B - going to Comcast coffers alone.

SIP anyone? 54% of business cable subscribers also use cable for voice, the report states. That means less than half the businesses using cable are buying voice from another provider. That is a shrinking opportunity for the 2000 Hosted VoIP players in the US.

"Last year the Cable/MSO share of businesses with 100+ employees rose to 17%, reports TNS. "The main driver behind this growth was a heavier reliance on internet service and the need for greater bandwidth; two areas where larger cable providers excel."

Telco broadband has not kept pace with cable in speed and price. Egged on by Google Fiber - and a declining market share of businesses - ILECs have started tentatively rolling out faster fiber based broadband - 100MB to 1Gigabit depending on the ILEC (Windstream versus CenturyLink or AT&T).

UPDATE: Google just rolled out Gigabit Fiber to small business starting in Charlotte in July of 2016.

The ILECs have made a tremendous CAPEX investment in TV - just as OTT TV is hitting its stride. They spent big to supply triple-play, when they could have spent the money on FTTx projects for faster bandwidth. That was just uncreative thinking. [More of that Me-too mentality ingrained in telco.]

All of this will stress ILECs, some CLECs and even some OTT VoIP players. When cable takes about 35% of the SMB market, there won't be much room left for anyone else.

In March of 2016, "During the fourth quarter, Verizon reported that total broadband connections dropped to 2.1 million as it lost more DSL subscribers after losing 94,000 DSL customers," according to Fierce media.

Verizon is transitioning. Verizon is now betting on mobile ads (AOL acquisition and Yahoo bid); 5G fixed wireless broadband replacement for wireline services; and IoT (including connected cars) to add to its coffers.

A point I make often is that the debt that the ILECs carry is crippling with flat revenues.

[

[Think about this: Vonage has taken $800M worth of voice revenue. Twilio gets $240 million in voice revenue. This is revenue that typically would go to Level3, Verizon and AT&T (and it probably does terminate to them eventually for a smaller percentage of that money).

WebRTC is being used in so many apps to allow for video and voice calls - bypassing the traditional voice network. [And bypassing the cellco text system and dollars.]

Then, we have Cable beating Telco in broadband bandwidth. Always has in fact. Gigabit fiber will be the real winner if the telcos decide to pursue that route for real (versus in just press releases).

We have telco getting in the data center - and now we have telcos looking to get out of that business without embarrassment.

There is a Talent problem, too. There are too many musical chairs. Not only can't you set a strategy when you shift personnel that much, you can't execute on a strategy either if the cogs are constantly being replaced. (And I don't mean cogs in a bad way. It takes a lot of talent to keep the wheels spinning.) The talent drain has also resulted in a domain knowledge drain as well. Quite frankly that means they don't where things are and how things have been done to keep things working. It isn't all documented, especially fiber maps!

Let's face it, for many companies that started with an A Team, they are now running with a B or C team. Why? As Steve Jobs said, "A Players hire A Players, B players hire C players. Get it?"

People move from company to company in teams. The same routine and team may work once, but it is not often a repeatable experience. There's a reason the Cavaliers recruited LeBron back to Cleveland - and didn't hire the whole Miami Heat starting line up.

The telco organizations harbor stifling factors: monopoly mindset, legacy systems, federal accounting and regulations, departmental silos and competing internal interests. These factors do not lend themselves to attracting more A Players.

There is also a surprising lack of talent for the new services and skills needed for omni-channel marketing; omni-channel customer service; cloud, managed services, migration and integration. This lack of skill will choke growth and brands.

We see outages and hacks every day. The worry is only about getting a customer. There is little concern for retaining that customer; data security; or a resilient network (4 Nines is good enough).

Many people are choosing smaller organizations to work for. The reasons are numerous but I would think that impact and voice play a major part. In smaller businesses, any one person can have a voice and can see the impact that they are having on customers, culture, and the company. That isn't the case in larger organizations.

Flat organizations (and smaller companies) have less meetings, fewer silos, maybe more transparent governance.

Most financial experts are predicting an economic slump in 2017. It won't matter which candidate wins the Presidential election, a slump is coming. We have under-employment; increasing number of freelancers; and a stagnant wage. None of these components inspire an economic engine that is fueled by consumer spending.

ARPU for cellular, cable and VoIP segments have been fairly constant over the last 4 years worth of data I could find. Bandwidth and voice revenues are actually shrinking. Total telecom spending from 2013 to 2014 shrunk $6 Billion dollars according to MarketResearch.

Growth will be hard to find. We are seeing a price war in cellular accompanied by escalating customer acquisition costs.

Hosted VoIP is experiencing a similar battle for customers that is increasing the cost of customer acquisition. Rising SPIFFs and other compensation are being used to grab both market share and channel partner attention.

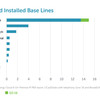

PBX vendors are NOT crashing and burning as many had predicted. Premise PBXs are still being sold and installed by a robust band of vendors - Mitel, Shortel, Avaya, 3CX, Fonality, Zultys, Panasonic, NEC, Siemens and more.

We are half way through 2016. No big winners. The Twilio IPO was a surprise. Vonage spending all of its acquisition money for the year on Nexmo, Twilio's competitor, seemed strange, since there were Broadsoft clients they could have picked off instead to take a big step forward in the race. Slack and all the Skype4B hype are little surprises.

2016 is half over - and so many companies have either done M&A or played musical chairs that I expect nothing magical to happen in the rest of 2016. And I look at all of this and wonder what 2017 holds.

ASIDE: telco versus cable consumer data.