So MITEL is getting bigger by buying Polycom. It had been rumored for weeks and now finally hits the news.

I wonder if Polycom saw the writing on the wall that the battle is going to come down to Microsoft versus Cisco? Motley Fool thinks that is why the OTT ITSP 3Some - 8x8, RC and Vonage - all had a bad day at the stock market. That would be funny, since who pays that close attention to the space? Not even analysts in the space really pay that close attention to detail.

Certainly, Skype for Business gets a lot of press. SfB is the Donald Trump of UC&C. But that doesn't mean that the OTT ITSP 3Some is going away - or won't add 20% revenue next quarter. There are other candidates for a company to use for UC&C, phones and dial-tone.

With the new Windows 10 update came a pin called PHONE on my laptop. So maybe there IS something to worry about.

The MS Connectors and Groups seems like MS is taking cues from Slack, even though SfB is integrated with Slack.

When the Fool says this: "RingCentral and friends are now facing challenges from Microsoft and many other titan-sized technology experts. The proof is in the pudding, and these VoIP experts must continue to show that they can deliver healthy business results in head-to-head competition with true giants." It makes me wonder if the Fool knows that the Giants ARE in VoIP -- Comcast, AT&T, Verizon. I mean, VZ has Cisco HCS, VCE, Broadsoft - and after buying XO will have more Broadsoft plus Genband.

Granted, no one is putting on seats as fast as SfB or Slack. And that, I think, is why the analysts are crying. In ten years of VoIP, it just hasn't crushed it yet.

I don't know if the analysts have looked, but customer acquisition is expensive - and hard - in VoIP. Far easier to include Lync with Office and Email than to try to sell it. Remember how MS included a shitty browser for free on the desktop? Or how they gave away Sharepoint?

VoIP Providers have to pay salespeople, build a channel, give away phones (and other hardware), SPIFFs, free months of service, just to get a customer. The cost of that acquisition is being questioned apparently on the stock market. OR it may all be a fluke and stock speculation going awry.

Either way, it doesn't shake the fact that the cost of acquisition is similar to cellular right now. The cellcos are buying customers for over $650 each!!! Imagine that!! The Street always watches the wrong numbers.

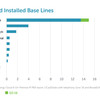

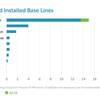

Meanwhile, in the handset market, Polycom probably peaked in market share at 38%. Yealink and many others are running into the space --- at the same time that many seats are being deployed without a handset! Softphones, mobile apps and even bluetooth headsets are taking market share from the handsets. Not just Polycom, but all of them!

This merger announcement was not taken well by many SPs. Fuze (formerly known as ThinkingPhones) has already announced inter-op with Yealink. A few others I spoke with are looking at Grandstream, Obihai and others -- because MITEL competes with them!

Now Windstream, AT&T and Verizon may not care with phone, because they sell MITEL and Avaya also. The rest of the players are tired of competing against their vendors! (BSFT should hear that last comment again and again!)

It wasn't even a good deal for Polycom. "The transaction will comprise $447 million in cash (23%) and $1.51 billion in stock (77%) and is expected to close in the third quarter of 2016. Mitel doubles in size--reaching revenue of $2.5 billion (2015 pro forma)--paying a relatively underwhelming 1.2 times trailing revenue (EV of $1.5 billion) and 7.3 times trailing EBITDA for a videoconferencing vendor," writes William Blair of Equity Research.

Also, Polycom's relationship with Microsoft for video was supposed to help Polycom's video business, especially for video enabled phones. I could see Microsoft relenting and using there own version of WebRTC to do video and calls inside Lync/SfB in the near future.

MITEL probably should have bought SLACK! By the time it closes this deal, Polycom won't be worth as much as it is now (diminishing returns).

There is a brave new world here. It is ruled by mobile apps - Facebook, Instagram. Snapchat, WhatsApp, twitter, Slack and others. (3 of those are owned by FB!) We know in the consumer play, FB has plans to be a trojan horse in payments and transactions. However, who takes the business desktop? So far it is Office365.

Cisco just launched Spark. It's integration with Salesforce is a highlight, but its ability to integrate with many other apps is why the folks at 170 West Tasman Dr. in San Jose think they will get some market share back. They are counting on Spark working well, the channel embracing it and the Cisco ecosystem still being valuable.

Customers buy ecosystem for integration, ease of use and sameness of GUI for the employees who utilize this stuff. Ultimately, BPaaS is where Spark is heading, with everything happening inside of Spark instead of a number of windows.

That is the one thing that MS and Cisco have: a certified channel that drinks the kool-aid. And these 2 companies are already ingrained in the Fortune 5000.

This space keeps getting interesting. The market thinks that MS/Cisco won already. You could say that Polycom cashing out admits defeat -- or the investors wanted the cash. Makes it harder for the ITSP market.