By now, most of us have heard that retailers such as CVS allowed NFC-based payments for a few days via Apple Pay and then blocked them in favor of QR-code based CurrentC by MCX. While retailers would prefer non-credit card-based solutions, such as MCX, these are the reasons CurrentC has already lost the war.

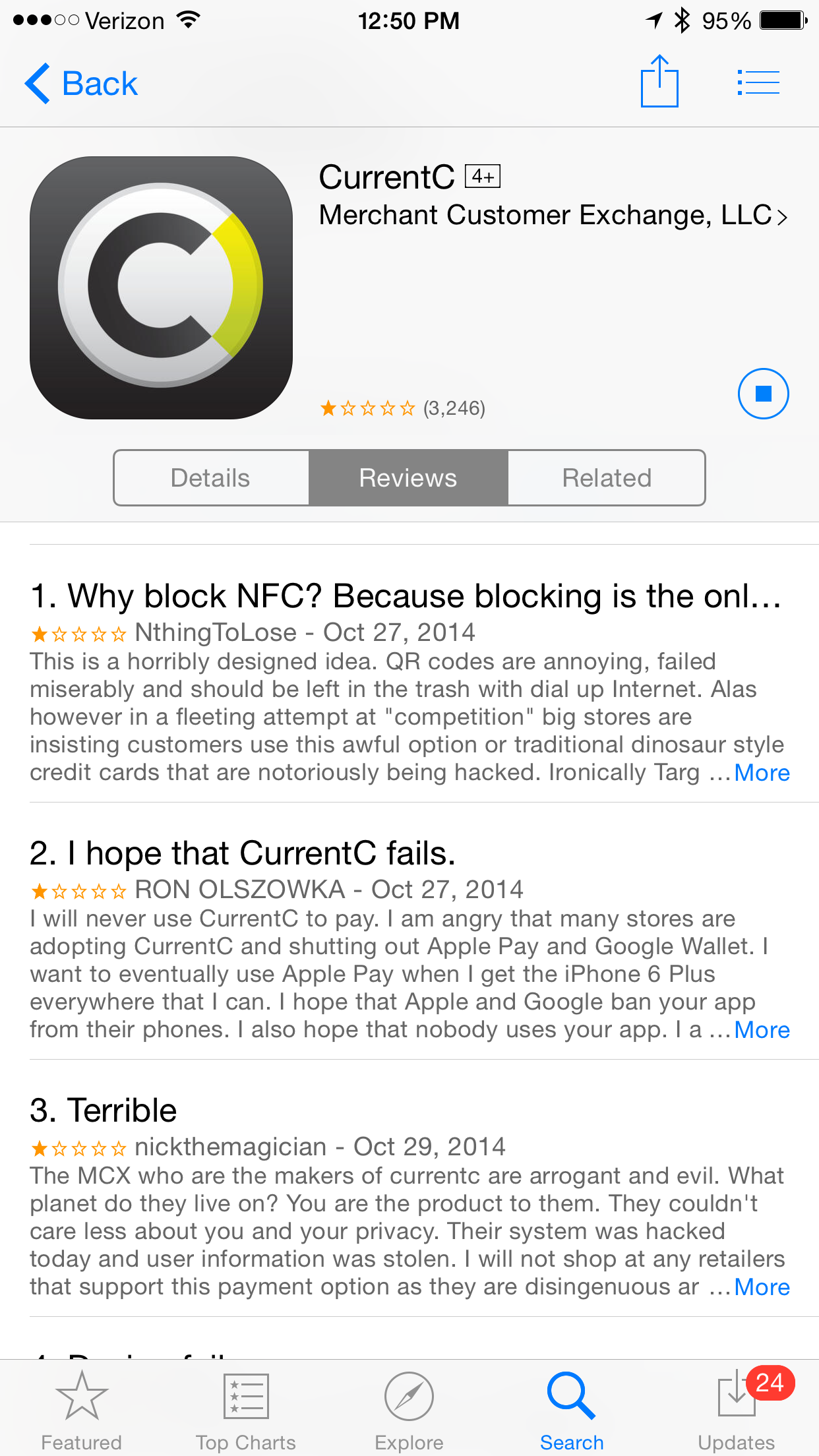

- There is a campaign to give the CurrentC app a one-star review and that is the number of stars it currently “enjoys.” Its top three reviews in the Apple iTunes App Store are horrifying as you can see above.

- CurrentC has already been hacked. Regardless of what was taken, the poor publicity will hound them.

- CurrentC requires access to bank accounts. No one wants to give away this information to a little-known company, moreover, see #2..

- CurrentC requires social security numbers. See #2.

- CurrentC uses QR codes which are less secure than NFC/fingerprint/biometric identification.

- CurrentC is more difficult to use than NFC-based solutions.

- Too many people don’t have bank accounts and need credit cards to be able to purchase. This is a large market that CurrentC can’t currently tap

- CurrentC may not be able to overcome the negative publicity associated with being the reason Apple Play has been blocked.

- CurrentC is way too late to market.

- CurrentC says they will embrace NFC if needed but may be too late.

In order for CurrentC to have become a major player, they would have had to launch one-year or more earlier. The technology they use has been around for many years so obviously, this wasn’t the issue. Moreover, to encourage use, they would have had to give consumers back something. For example, a 2.5% savings on all sales for one-year might have cemented their position as a solid credit card alternative.

In fact, helping retailers avoid the 2-3% credit card fee is exactly the reason this company is gaining traction. But while retailers would love to take the credit card companies out of the purchasing equation, plastic offers many benefits such as favorable dispute resolution which consumers love. Then there is the matter of cash back, miles and points which consumers are already used to accumulating when they shop using cards.

In other words, now that alternatives exist, and they are getting easier, it is too late to get consumers to accept a QR-based system that takes credit cards out of the equation. If CurrentC evolves and takes my cash-back idea, things may get more competitive. For now though, Apple Pay and to a lesser extent, Google Wallet will be the major players in the space and retailers will likely have to buckle to consumer pressure to support these systems

If you’re looking for more good information on the topic of Apple Pay and why it will be successful, check out this Seeking Alpha article. Gary Kim also has some solid thoughts on the matter as well.